UPDATE 9/23/16: The governor has signed California’s Child Credit Freeze Legislation AB 1580. California parents can now freeze their child’s credit!

My first-ever NewsMom blog was titled “Why My Toddler Has a Credit Card.” Six (long) months later, I followed that up with “How I Forced The Bureaus To Freeze my Child’s Credit” and “A Step-by-Step Guide To Freeze Your Child’s Credit.”

Needless to say, the topic of child credit freezes is one that is near and dear to my heart… and it seems persistence may soon pay off.

Citing these NewsMom blog posts, this week California Assemblyman Mike Gatto introduced the child credit freeze legislation AB 1580. For the first time, it would give California parents the right to freeze their child’s credit and utilize the single best tool to prevent financial ID theft.

A credit freeze basically prevents anyone from running a credit check using your Social Security number. Without a credit check, crooks should not be able to take out credit in your name (credit cards, loans, etc.). If you need to take out a loan or open a credit card, you simply call or log on to the bureaus’ sites, and temporarily “thaw” your credit freeze.

The Legal Loopholes

California was the first state to pass a law requiring the bureaus to allow “consumers” to freeze their credit. As other states began to follow suit, the bureaus decided to “voluntarily” allow consumers in every state to freeze their credit. Fifty states and the District of Columbia have now enacted various versions of credit freeze laws.

However, while Equifax will now allow you to freeze your child’s credit in any state, the other two bureaus—Experian and TransUnion—still refuse unless it is mandated by state law.

The primary issue, according to the bureaus, is that most kids don’t have a credit file to freeze unless they’re already a victim of ID theft. Unlike Social Security numbers that are issued at birth, children do not build a credit file until they actually start using credit.

In order to place a freeze on a child’s Social Security number, the bureaus would have to create a “file” to freeze.

Studies show children can be even more desirable ID theft targets than adults, and it’s estimated that tens of millions of kids were compromised in 2015 alone through massive insurance and government data breaches.

As of December 2015, 23 states have updated their laws to require that the bureaus allow parents to freeze their child’s credit before they become a victim. Until now, California was not one of those states, and it seemed lawmakers and regulators simply didn’t care.

Lawmaker Apathy

When I first began reporting on the topic in 2014, I contacted California Attorney General Kamala Harris’ office… repeatedly. Harris had just held a press conference on the dangers of ID theft (leading up to the midterm elections).

Naturally, I assumed her office would jump at the chance to ensure that children in California had the same protections as those in 18 other states (at the time). I’m still waiting for a response.

I then reached out to several state and federal lawmakers, who feigned interest in child credit freeze legislation but never followed though.

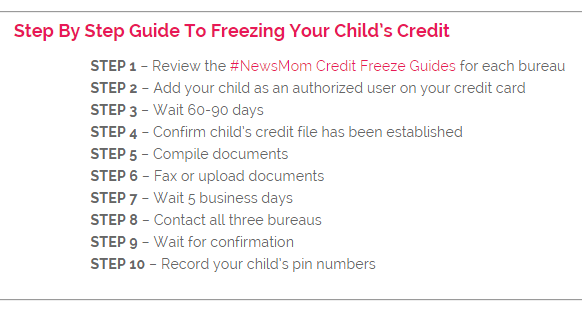

So, I found a loophole of my own and came up with a work-around that allowed me to freeze my daughter’s credit. I spent nearly a year going back and forth with the bureaus and ultimately compiled this step-by-step guide to help other parents.

Click Here For The Complete Guide To Freezing Your Child’s Credit

But bottom line, it shouldn’t be this hard.

Then yesterday, I got word from Gatto’s office that they introduced AB 1580.

Little Opposition

Generally, when a lawmaker introduces legislation, it doesn’t make news because we know it’s likely to be rewritten or killed in committee. But Gatto’s team tells me they expect little opposition as the bureaus have already weighed in and AB 1580 is similar to existing child credit freeze legislation in other states.

However, now that I’ve had the opportunity to read the bill’s text, I am concerned that it requires parents to submit the documents needed to prove guardianship “to the address or other point of contact and in the manner specified by the consumer reporting agency.”

In other words, the bureaus get to decide how and where you submit your request for a child credit freeze.

As I outlined in “How I Forced the Bureaus to Freeze my Child’s Credit,” two of the three bureaus ask parents to mail sensitive information (copies of Social Security cards, a birth certificate, driver’s license, etc.) to a P.O. Box. The address on the envelope is enough to tip off bad guys that there’s an entire identity inside, and you can’t send FedEx or registered mail to a P.O. Box.

The bureaus eventually provided me with internal fax numbers to submit my daughter’s documents and agreed to let me share them here in “A Step-by-Step Guide to Freeze Your Child’s Credit.” However, the bureaus should provide a more secure option for every parent, not just NewsMom readers.

The line quoted above seems to be standard language in most of the other state child credit freeze laws, including Arizona, Delaware, Florida, Georgia and Indiana, just to name a few.

I’ve pointed this out to Gatto’s legislative team, and you can count on follow-up posts and TV news stories as the bill makes its way though committee.

Extending Child Credit Freeze Rights Nationwide

Last year, as I was going round after round with media reps at all three bureaus, Equifax had a change of heart and agreed to voluntarily extend the child credit freeze right to parents nationwide.

While Experian and TransUnion still refuse, many believe this California child credit freeze legislation is one large step toward giving parents the same rights nationwide.

After all, it was a California law that ultimately led to the bureaus voluntarily allowing “consumers” to freeze their credit. As Gatto pointed out in an interview last year, “You know, if California acted, one-tenth of the population would have this protection and we’d probably get a federal law.”

In a separate interview, the Federal Trade Commission’s David Newman agreed.

“It’s something that ought to be a national policy,” said Newman. “It’s such a good idea and so simple to do. If one credit reporting bureau can do it, the others can. If 19 states can do it, the rest can too.”

Needless to say, the experts agree that this should be a federal law… and one has been introduced.

Rhode Island Congressman James Langevin introduced H.R.1703 – Protect Children from Theft Act of 2015 last year. Not only would it amend the Fair Credit Reporting Act to allow all parents to freeze their children’s credit, but it would also direct the “Consumer Financial Protection Bureau to: (1) establish implementing procedures, and (2) determine what fee, if any, may be charged by a consumer reporting agency to create, convert, or unblock a file.”

In other words, all parents would have the same rights and the CFPB could require a more secure method for submitting sensitive information to the bureaus.

However, the federal legislation was introduced nearly a year ago and was sent to the House Financial Service Committee where it is still waiting to be heard. I’m told it’s nowhere on the schedule and there is still no ETA.

Stay tuned…

For more information on how to detect, repair and prevent child ID theft, see:

#NewsMom Research & Resources – Child ID Theft

qzonzy

h9uhye

2xmw1k

cc1syh

0g1qmq

dryph0

cyp179

wj6oi2

6n2mbu

3tny02

4p1sjs

ldt9iv

95nlex

jhty4v